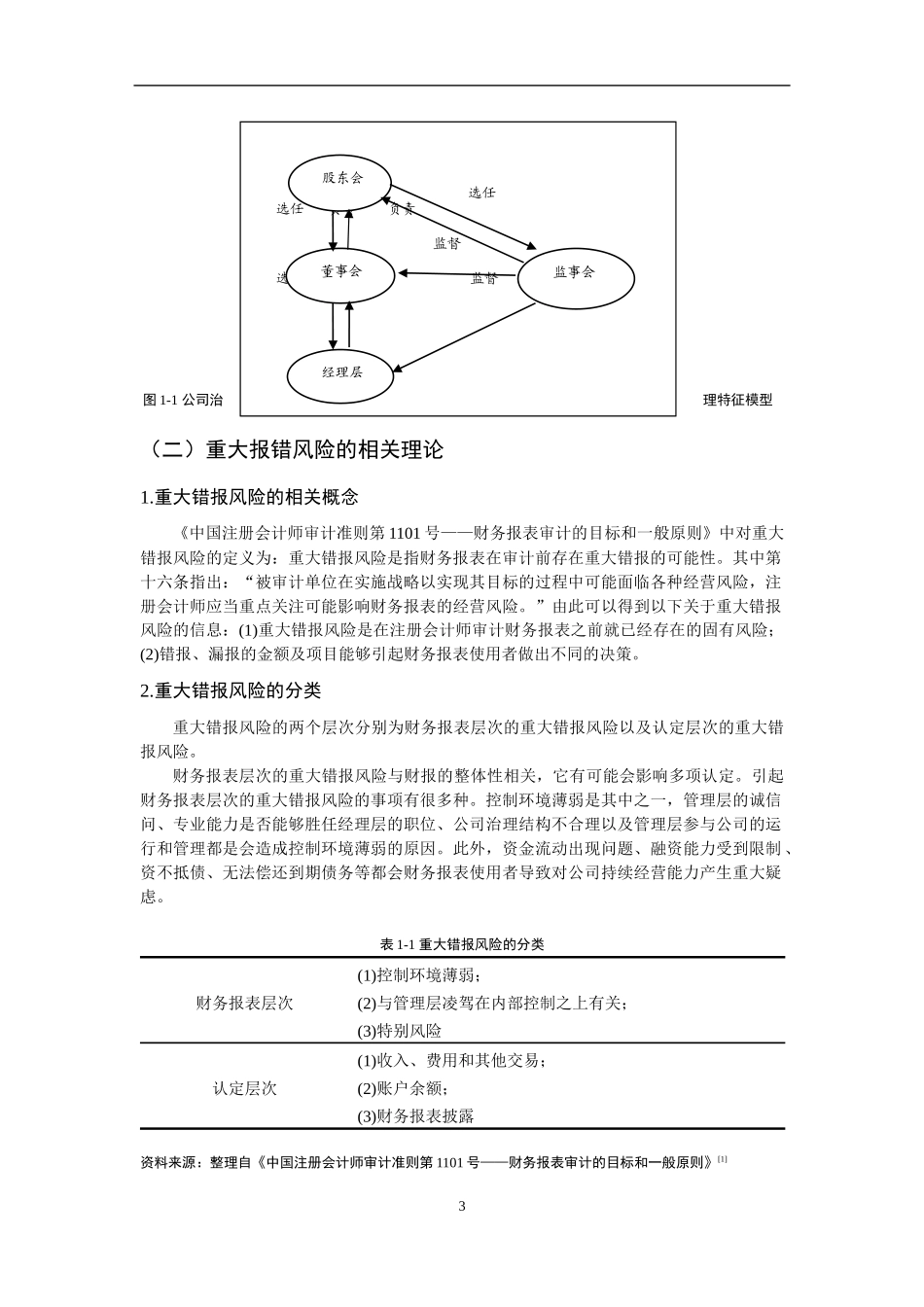

公司治理特征与审计重大错报风险关系研究摘要:目前,我国审计环境复杂性日益增加。注册会计师在审计被审计单位时对于重大错报风险的识别和评估的难度也日益增加。现阶段,我国上市公司治理还处于发展不成熟的阶段,相对应的财务指标存在一定的差错,审计人员所面临的审计风险加大,新审计准则将评估和识别重大错报风险作为审计程序起点,因此加深对于公司治理特征与审计重大错报风险关系的理解是十分重要的。本文是在综合考虑我国上市公司发展现状基础之上,结合被证监会处罚的财务舞弊公司的状况,沿着公司治理这条主线,研究公司治理特征对审计重大错报风险的影响以及它们之间的相互关系。本文研究了不同治理特征下带来的审计难度,考虑了股权结构、董事会、监事会三种公司治理特征下导致重大错报风险增加的原因,以此为依托指出了财务信息失真的内因,并提出了对应的对策。这对避免审计人员由于双方信息不对等所造成的审计失误有非常重要的意义。关键词:公司治理特征;重大错报风险;违规Study on the relationship between the governance characteristics of listed companies and the risk of audit major misstatementsAbstract: With the increasingly complex audit environment, the difficulty of identifying and assessing the risk of major misstatements in the process of audit has gradually increased. At the present stage, Chinese corporate governance efficiency is low, Financial information is seriously disordered, and the audit litigation responsibility increases. Modern audit model and new auditing standards introduced, The starting point of audit procedures is that assess and identify the risk of material misstatement. So understanding plays an important role in corporate governance characteristics and audit risk of material misstatement. This paper is based on a comprehensive consideration of the current development of Chinese listed companies, combined with the punishment by the Commission of financial fraud. Along with corporate governance, this paper studies the relationship between governance ch...